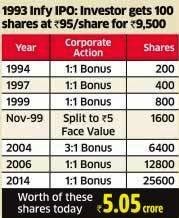

In the world of investments, one is constantly barraged by data, analyses, news, etc., As we saw some issues back most of it is noise, and only few signal. Indeed, the investment world is the most famous one after entertainment with dedicated news channels, newspapers etc.

The management thinker Stephen Covey said that the only way to take on big tasks is to first start within your circle of competence and slowly expand your competence, Most of the time we end up doing the opposite in investing. A civil engineer buys stocks of IT companies without much knowledge of IT companies working, whereas the guy in IT co may be buying the stock of the engineering co because some talking head on TV said it was a good ‘buy’. So the first thing is to look for investment opportunities within your circle of competence, So first gain knowledge of the companies you work for, suppliers , competitors, customers etc.

In the last 4-5 years compared to any other industry FMCG Co’s have given stellar returns, this would have been obvious to any FMCG employee, supplier, stockist etc.; I’m not sure how many used this information. Obviously I’m not asking the FMCG employee to bet his house but buy the co’s share because he is the first one to see the growth that I would be the last one to see.

Normally as they say grass is green on the other side, hence many do not invest in their own co’s but that of others!

The above is the first level of competence, second level is where we as consumers come across great products that we use daily. Let us see some of the products:

Toothpaste and Brush : Colgate, Hindustan Uniliver, P&G

Water Purifiers: Tata, HLL

Kitchenware: Hawkins, Prestige

Appliances: Bajaj Electricals, Whirlpool,

Breakfast: HLL from cookies to bread,

Watches and Jewelry: Titan

Footwear: Bata

School Books, Note Books, Stationery: NAvneet, ITC,

This is just before 9 AM!!

We can go through this the entire day Transportation, Food, Medicines, even Holidays!!

The above does not obviously mean that all these are great companies to invest in but they are the starting point for further study, into the company & the environment it operates on.

So there is wealth out there, for many of us though this may be too much work to research and buy, o buy only in your circle of competence and leave the rest to professionals like Mutual Fund managers who scour the market for good investments every day. Some of them have compounded wealth so well that as I wrote previously, if you don’t want to go through this work, it is as easy as fill it shut it forget it to invest and reap rewards from long term investing via equity mutual funds.

Of course you need to comply with your co’s rules on insider trading. We need to distinguish between genuine research and insider trading, Calling your friend and telling him that your co’s board has approved a rescue plan before anyone in markets know it is insider trading, which is what Rajat Gupta is alleged to have done, but doing your homework in analyzing a co whether it is where you work or its product is liked by you or your friends is not insider trading.